SBI versus HDFC Lender against ICICI Bank: Mortgage prices opposed – Take a look at which provides you with most readily useful EMIs

It may be a little difficult, when you are in the middle of settling financial. Any month-to-month costs are moved on because monthly you have to keep spending EMIs.

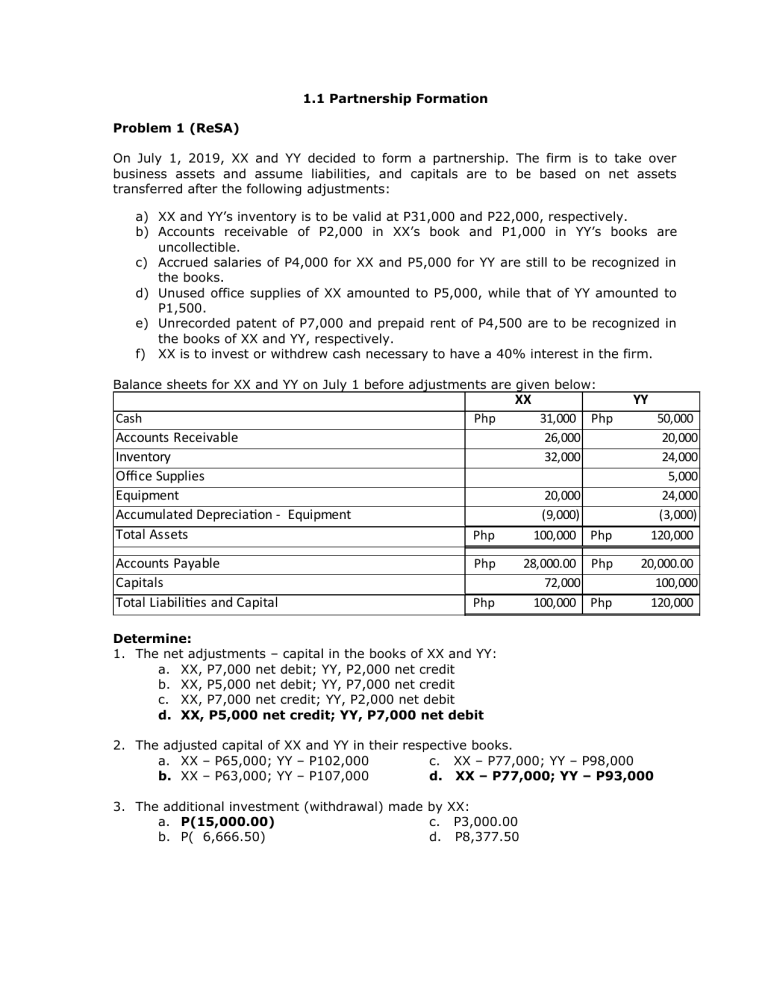

Condition Bank from Asia (SBI) produced our home financing less expensive by detatching the new MCLR by 5 more affairs if you’re to present the Q4FY19 influence. It was second-cut by SBI since the RBI’s monetary policy. New flow would reduce the eye costs, permitting individuals. However,, the home loan individuals create work for probably the most because the EMIs perform become decreased, which have SBI’s interest rate coming down from the 15 base facts since . This flow tend to in person benefit the borrowers of SBI. Not surprisingly, it will always be best to examine. Whenever home loan interest rates try all the way down, the monthly EMI is also low priced which provides much more independence during the paying down expenses.

First off, let us examine SBI that have several almost every other grand loan providers – HDFC Bank and you can ICICI Lender. In the place of the official-had lender, additional two individual lenders was but really to help you declare any transform in their home financing interest levels.

SBI – With effect out-of , SBI’s home loan less than Rs 29 lakh, is now offering rate of interest ranging from 8.55% to eight.75% to have salaried women and you can 8.60% to 8.75% to possess salaried people. Meanwhile non-salaried people gets rates ranging from 8.70% to 8.80% and you may 8.75% to 8.85% respectively.

Having mortgage significantly more than Rs 30 lakhs however, upto Rs 75 lakhs, SBI’s interest rates stands regarding 8.80% to 8.90% with the salaried ladies and 8.95% to nine.05% on non-salaried people. While you are interest rate towards the salaried people today applies ranging from 8.85% to 8.95%, for low-salaried within group would-be charged with rates out of 9% in order to nine directory.10%.

Over Rs 75 lakh home loan, salaried consumers will get rates between 8.90% so you’re able to nine.05% in addition to men and women. While, the fresh non-salaried ones will have nine.05% so you can 9.25% rates.

HDFC Financial – To have mortgage upto Rs 31 lakh, the bank levies interest rate off 8.70% and 8.75% into the salaried women and men correspondingly. If you’re if one is actually mind-functioning then, price could be 8.85% and you can 8.90% into the gents and ladies.

Mortgage brokers between Rs 29 lakh to help you Rs 75 lakh, provides prices out of 8.90% on the salaried women and you will 8.95% with the salaried people. In case there are care about-operating, this new pricing try 9.05% and you will 9.10% respectively.

A lot more than Rs lakh, rate of interest is set at the 8.95% and you can nine% on the salaried people, whereas rates from 9.10% and nine.15% is offered on the notice-employed.

ICICI Financial – Here an excellent salaried borrower becomes 9.05% interest rate towards home loan upto Rs thirty-five lakh, whenever you are 9.15% and 9.20% is decided on loans anywhere between Rs thirty-five lakh to Rs 75 lakhs and over Rs 75 lakhs.

If you’re, a personal-functioning mortgage borrower will have to shell out nine.10% rate of interest if loan taken fully to Rs 35 lakhs. When you’re, loan anywhere between Rs thirty-five lakhs to help you Rs 75 lakhs have an effective rates of 9.20% and you will a lot more than Rs 75 lakh features nine.25% rate.

MCLR are a benchmark put by the RBI, less than and therefore a bank never give. And that, MCLR will be a shield to own finance companies that they must lend be personal loan, car loan or financial over the benchmark. The difference between home financing floating speed and you may MCLR is actually known as give that’s up to the bank to choose. And thus, when MCLR gets cut every financing linked to it is going to get a hold of loss in their attention prices and therefore EMIs.

not, rather the present consumers will be unable to enjoy the newest loss of rates on account of MCLR. Such as in case there is SBI and ICICI Financial, he has connected their house loan having 1-year MCLR. Therefore eg, when you have removed a home loan for the and is connected with 1-seasons MCLR, who would mean the fresh new enhance in their prices was seen during the no matter what alterations in the newest standard when it comes to those period. But not, the brand new consumers really can enjoy the rates incisions. Which have MCLR slashed, EMIs also needs to see a comparable way.

Who also provides most readily useful EMIs? An example

When you yourself have picked SBI mortgage upto Rs 30 lakh for a tenure out of two decades on mortgage away from 8.55%. Then your desire on the financial carry out amount to Rs dos,71,130 lakh also principal amount of Rs 29 lakhs. You are going to spend EMIs regarding Rs twenty six,129 per month.

However if when the already pulled HDFC Bank financial at same matter and period, however with an interest rate away from 8.70%. Your desire number was at over Rs 3.39 lakh along with dominating quantity of Rs 30 lakh. If you find yourself EMIs you will pay per month was Rs twenty-six,416.

While from the ICICI Bank mortgage upto Rs 29 lakh that have period regarding twenty years from the mortgage out-of 9.05% can lead to way more EMIs. According to the calculator, their focus carry out already been over Rs step 3.50 lakh and principal count. For their EMIs, they’d getting more Rs 27,100000.

As, SBI trim down its MCLR this new impression is known within the home loan interest levels and make the EMIs less compared to HDFC Bank and ICICI Financial. It would be interesting to view, whether the most other one or two individual loan providers can make a similar move to remain afloat in the competition.

Taxation Benefit on the mortgage:

It could be some burdensome, when you are in the course of settling home loan. All of your current monthly expenditures was shifted due to the fact per month you may have to continue paying EMIs. Although not, one of the biggest great things about home loan could be the income tax work with it comes down having. Considering area twenty four of cash Taxation Operate, an individual may allege limitation Rs dos lakh tax benefit into the financial appeal paid back in the event the their residence was mind-filled. Concurrently, less than section 80C there clearly was already a taxation claim away from Rs 1.5 lakh on principal number. And that, you’ve got the opportunity to stop their home mortgage weight.